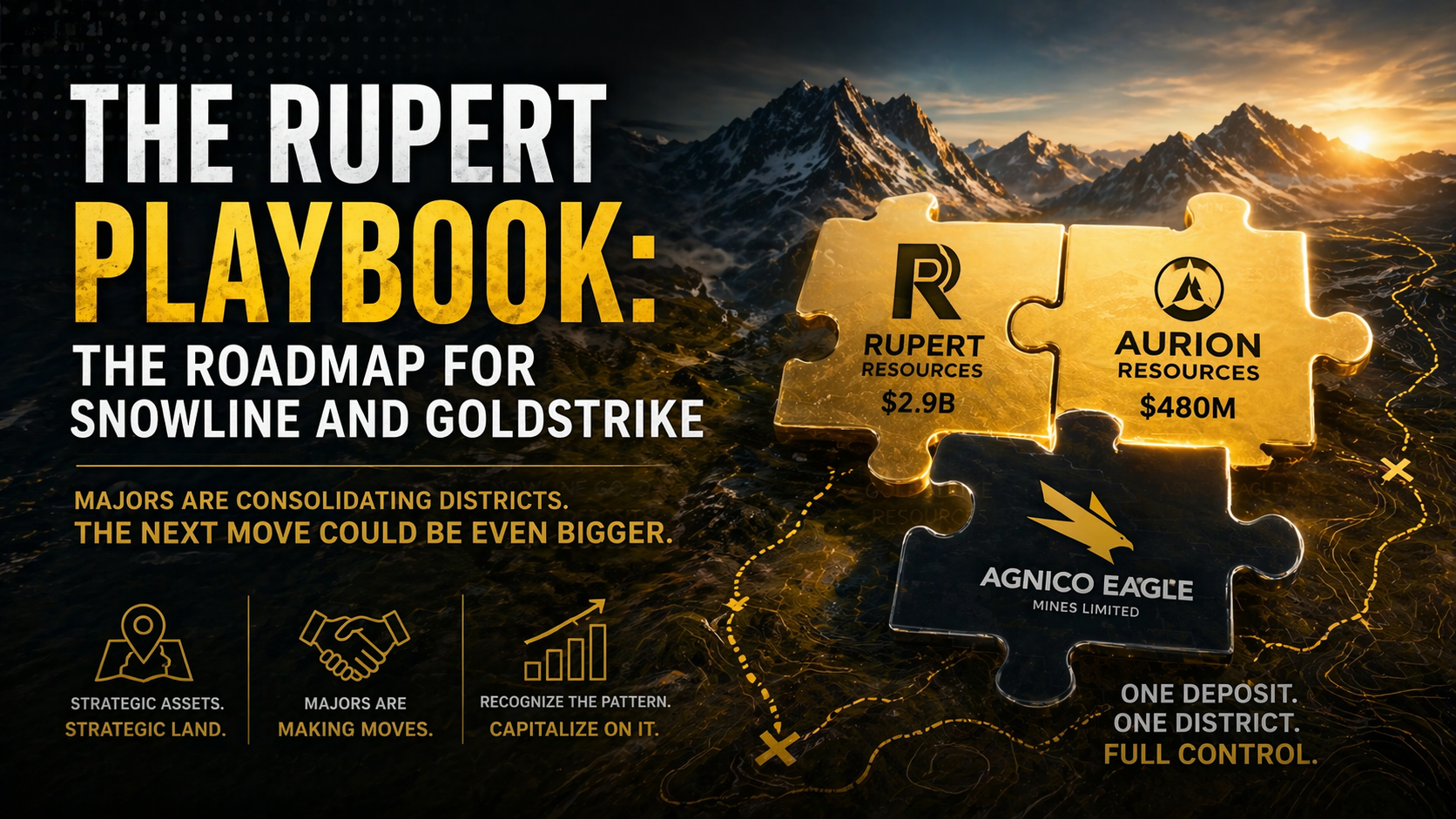

This week, Agnico Eagle Mines (NYSE: AEM, TSX: AEM) dropped one of the most important M&A stories in the junior gold sector in years.

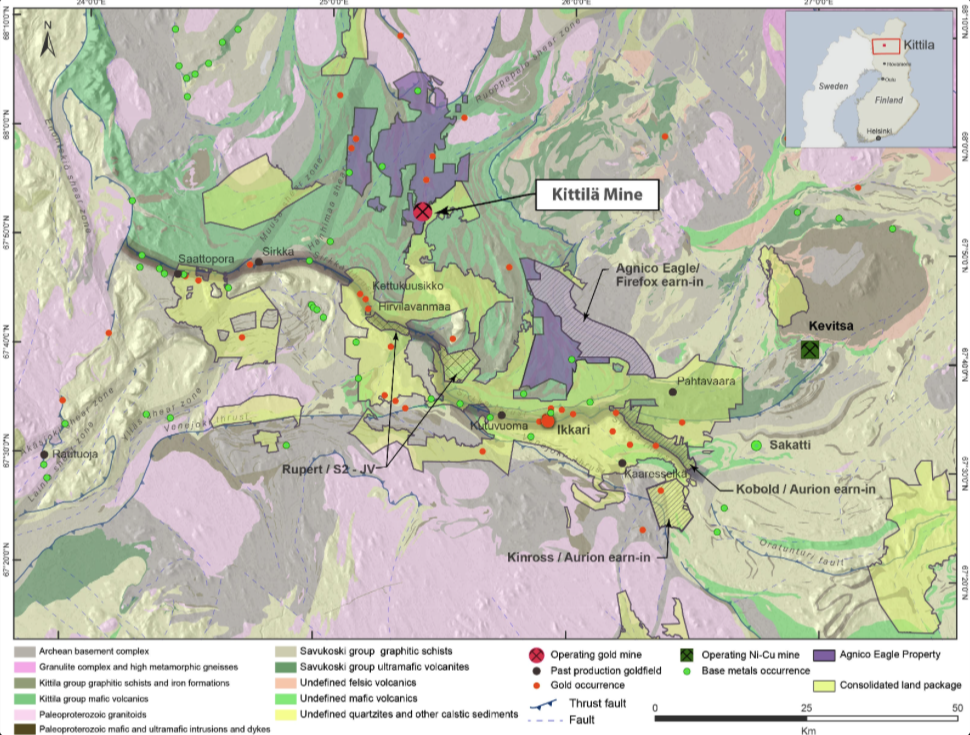

On April 20, 2026, the Canadian major announced it is acquiring Rupert Resources in a deal valued at approximately C$2.9 billion (share consideration plus contingent value rights) and Aurion Resources for C$481 million in cash. A separate deal for B2Gold’s stake in a joint venture rounds out the package, giving Agnico full control of a massive land position in Finland’s Central Lapland Greenstone Belt.

Rupert owned the high-quality Ikkari gold project, a large, advanced-stage deposit that anchors the deal. But here’s what makes this transaction so instructive: Aurion didn’t even have a resource estimate. What it did have was a large, strategic land package surrounding Rupert’s assets. For years, Rupert downplayed the need for that ground. Agnico clearly disagreed. By buying both companies at once, the major secured not just the deposit, but the entire district-scale opportunity around it.

This is classic major-miner behavior in a high-gold-price environment. With their own shares trading at premium valuations after a strong run, companies like Agnico are using their currency to scoop up undervalued juniors and build pipelines without the risk of greenfield exploration. And they’re doing it aggressively, paying premiums to lock in surrounding land rather than fight over it later.

Why This Matters for Gold Strike Resources (TSXV: GSR)

Look at the Yukon’s Tombstone Gold Belt and you see an almost identical setup unfolding right now.

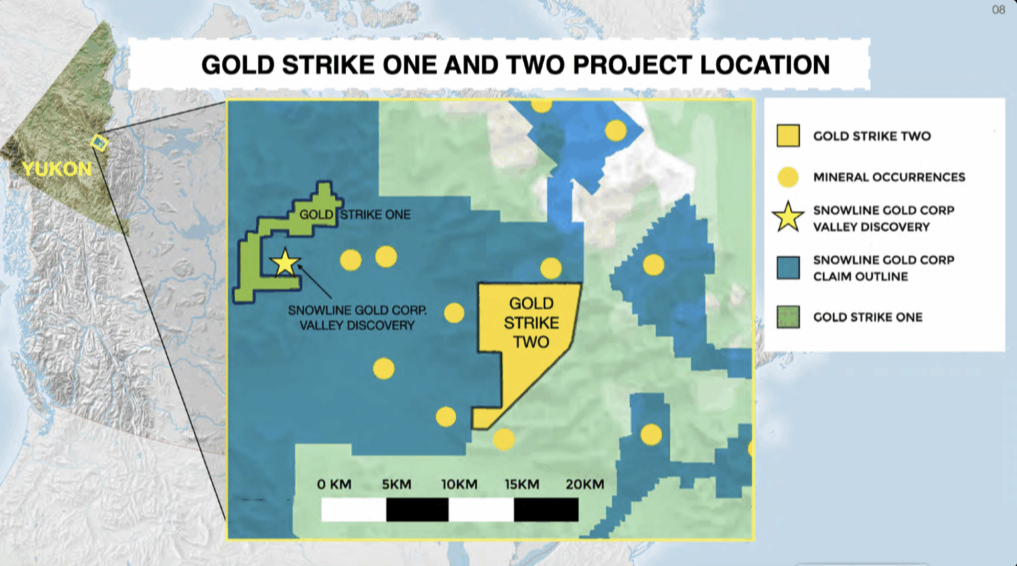

Snowline Gold controls one of the most compelling undeveloped gold deposits on the planet: the Valley deposit on its Rogue Project. The latest resource estimate shows 7.94 million ounces in the Measured & Indicated categories at 1.21 g/t Au, plus another 0.89 million ounces Inferred, roughly 8.8 million ounces total. It’s a high-grade, bulk-tonnage Reduced Intrusion-Related Gold System (RIRGS) with outstanding metallurgy and economics.

But to turn that into a mine, Snowline will need infrastructure: roads, water management, tailings, and access corridors. And right now, much of the critical surrounding land sits with Gold Strike Resources.

GSR’s Gold Strike One project sits immediately adjacent to Snowline’s Valley discovery, its southern boundary is less than 500 metres from the southern extent of the interpreted resource pit. Gold Strike Two adds more ground to the east. Combined with GSR’s recent acquisition of the Florin Gold Project (2.5 million ounce inferred resource) and other claims, the company now holds one of the largest consolidated land positions in the entire Tombstone Belt.

Here’s the visual parallel:

Rupert’s Ikkari project (core asset) surrounded by Aurion’s land. Agnico bought both to consolidate the district.

Snowline’s Valley discovery (yellow star) literally wrapped by Gold Strike One (green) and Gold Strike Two (yellow). The adjacency is striking.

The lesson from Finland is crystal clear: when a major decides to develop a tier-one asset, it doesn’t want to risk years of permitting delays, legal battles, or infrastructure bottlenecks caused by fragmented land ownership. It’s far cheaper, and far smarter, to pay a premium and own the entire district outright.

For a $100-billion-plus company like Agnico (or any other major eyeing the Yukon), acquiring Gold Strike’s land package would be pocket change in the context of building a multi-million-ounce mine. But for GSR shareholders, it could mean a transformative premium.

The Bigger M&A Wave Is Just Starting

Gold remains elevated, majors are cashed up and trading rich, and the pipeline of high-quality undeveloped assets is thin. The Rupert/Aurion transaction is not an isolated event, it’s a signal. We’re entering a period where district-scale consolidation becomes the name of the game.

Snowline’s Valley is exactly the kind of asset majors covet: scale, grade, jurisdiction, and metallurgy all in one package. When the inevitable bid comes, and most observers believe it’s only a matter of time, the buyer will almost certainly want the surrounding ground too.

Gold Strike Resources is that ground.

The company already has scale (thanks to Florin), fresh capital from its recent $15 million bought deal, and a land position that is strategically irreplaceable. The market hasn’t fully appreciated this yet. But the Finland deal just handed every investor a roadmap of exactly how these situations play out.

Those who connect the dots early between what just happened in Finland and what is quietly setting up in the Yukon, are the ones who stand to make the most when the next chapter of this story writes itself.

DISCLOSURE: The author did not receive any compensation for publishing this article. The author holds a position in Goldstrike Resources Corp and may choose to buy or sell shares of the company at any time without notice. The author does not hold positions in any of the other companies mentioned. While reasonable efforts have been made to ensure the accuracy and reliability of the information provided, readers are encouraged to conduct their own research and seek independent financial advice before making any investment decisions related to the companies discussed