The AI boom is clearly not slowing down.

Once again, NVIDIA delivered a monster quarter, proving that AI infrastructure spending is still one of the strongest themes in the market. Companies are spending billions building AI data centers and demand still seems completely out of control.

What I actually found most interesting though was not even the earnings themselves.

NVIDIA announced an enormous $80 billion buyback alongside a dividend hike. To me, that feels like a pretty major shift. NVIDIA is starting to transition from a hyper-growth rocket ship into more of an AI blue-chip giant.

And when that happens, risk capital usually starts looking further downstream for the next layer of the trade.

Everyone already owns the mega caps.

That is exactly why I started looking deeper into Applied Optoelectronics ($AAOI).

I completely missed the huge runs in SanDisk and Micron Technology as investors realized AI infrastructure demand was much bigger than expected. I did not want to miss the next phase of the trade.

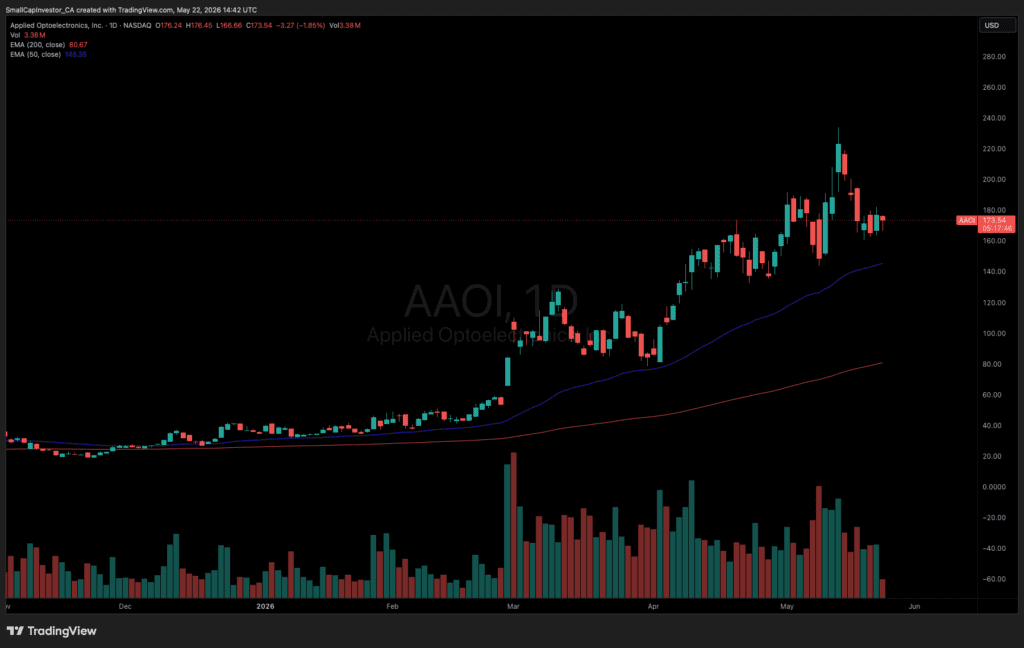

So I decided to start building a position in AAOI around the $170 level.

The reason is simple.

AI is not just about chips anymore.

Everyone focuses on NVIDIA GPUs, but these AI data centers are basically giant digital factories and all the GPUs need to communicate with each other insanely fast. At a certain point, the bottleneck stops being chips and becomes moving data fast enough.

That is where AAOI comes in.

The company makes high-speed optical networking products that help connect AI servers and hyperscale data centers together. In simple terms, NVIDIA may provide the brains of AI, but companies like AAOI are helping build the highways those systems communicate through.

And right now, demand looks completely insane.

AAOI just reported record Q1 2026 revenue of $151.1 million, up 51% year-over-year and marking the company’s fourth straight record quarter. Even more impressive, data center revenue surged 154% year-over-year to $81.4 million and now makes up more than half of total company revenue.

Management says demand is now “significantly exceeding capacity through at least mid-2027.”

That is a massive statement.

The issue is no longer whether demand exists. The issue is whether the company can actually manufacture enough product fast enough to keep up with the AI buildout happening across the world.

Management recently raised full-year 2026 revenue guidance to more than $1.1 billion while expecting over $140 million in non-GAAP operating income.

To put the growth into perspective:

| Year | Revenue |

|---|---|

| 2024 | ~$456M |

| 2025 | AI ramp really starts |

| 2026 | >$1.1B guided |

Those are the kind of numbers that can completely re-rate a stock.

What also makes the story interesting is who AAOI is supplying.

The company already has volume 800G shipments underway while next-generation 1.6T products are currently being qualified with hyperscalers including Amazon, Microsoft and Oracle. Recent orders include a $71 million 800G order that was upsized in April alongside a previously disclosed $200M+ 1.6T deal.

That is why the story matters.

The first phase of the AI boom was buying GPUs.

The second phase was memory and storage plays like Micron and Sandisk.

Now it feels like the market is moving toward the networking and optical connectivity layer powering these massive AI data centers.

AI models are getting bigger, data centers are getting bigger, and the amount of data moving around these systems is exploding. That is why companies tied to networking and optical connectivity suddenly matter a lot.

And AAOI is positioning aggressively for that future.

The company is rapidly expanding manufacturing capacity in Texas, including new facilities in Sugar Land and Pearland. Management says production capacity could exceed 650,000 800G and 1.6T units per month by the end of 2026 and more than 930,000 units per month by the end of 2027.

Interestingly, roughly 40% of this production is expected to happen in the United States.

That could end up becoming a major advantage as governments and hyperscalers increasingly prioritize domestic supply chains and U.S.-based AI infrastructure manufacturing.

The other thing bulls love about AAOI is the vertical integration story.

Unlike many competitors, AAOI manufactures much of its technology internally, including lasers and optical components. That gives the company more control over production and supply chains during what is turning into a full scale AI infrastructure arms race.

There are definitely risks here.

AAOI is still approaching consistent profitability and execution on the Texas manufacturing ramp is critical. If the expansion slips or demand cools off, the stock probably gets hit hard. The company also has customer concentration risk and has previously relied on equity raises to fund expansion.

But in a full AI supercycle, I can absolutely understand why some investors think this story could still have another major leg higher.

At roughly a $14 billion market capitalization, AAOI is obviously not “cheap” anymore. But based on management’s updated 2026 revenue guidance, the stock is trading closer to roughly 12-13x forward sales rather than the much higher trailing multiples many investors focus on.

And if the company successfully ramps from roughly $1.1B revenue in 2026 toward several billion dollars annually over the next few years as 1.6T adoption accelerates, the market starts valuing the company completely differently.

I believe AAOI could eventually become a $100B+ market cap company if it captures a meaningful share of the AI optical networking market during this cycle.

That sounds crazy today.

But so did many of the moves in NVIDIA, Micron, Super Micro and other AI infrastructure winners before they went vertical.

The bigger takeaway here is that the AI trade is evolving.

This is no longer just software hype or chatbot excitement. This is turning into a full scale infrastructure arms race involving chips, networking, optical connectivity, power and massive data center expansion.

And increasingly, the market is rewarding the companies helping build that backbone infrastructure.

DISCLOSURE: The author did not receive any compensation for publishing this article. The author holds a position in Applied Optoelectronics and may choose to buy or sell shares of the company at any time without notice. The author does not hold positions in any of the other companies mentioned. While reasonable efforts have been made to ensure the accuracy and reliability of the information provided, readers are encouraged to conduct their own research and seek independent financial advice before making any investment decisions related to the companies discussed